Data & SourcesHow we can consistently provide accurate, verifiable data.

Bizminer data is sourced from the top reliable public, private, and web statistical data sets.

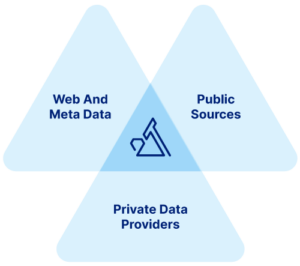

Our Trusted Data Sources & Partners

Bizminer sources over 1 billion data points from 18M+ business operations.

We synthesize raw data points from reliable, diverse sources to generate final measurements for our profiles and reports.

Use Our Data at Your Organization

Schedule a 1:1 conversation today to learn how organizations like yours have used an API integration to incorporate our data into essential applications, reports, and workflows.

Our Methodology: More Data, More Reliable Insights

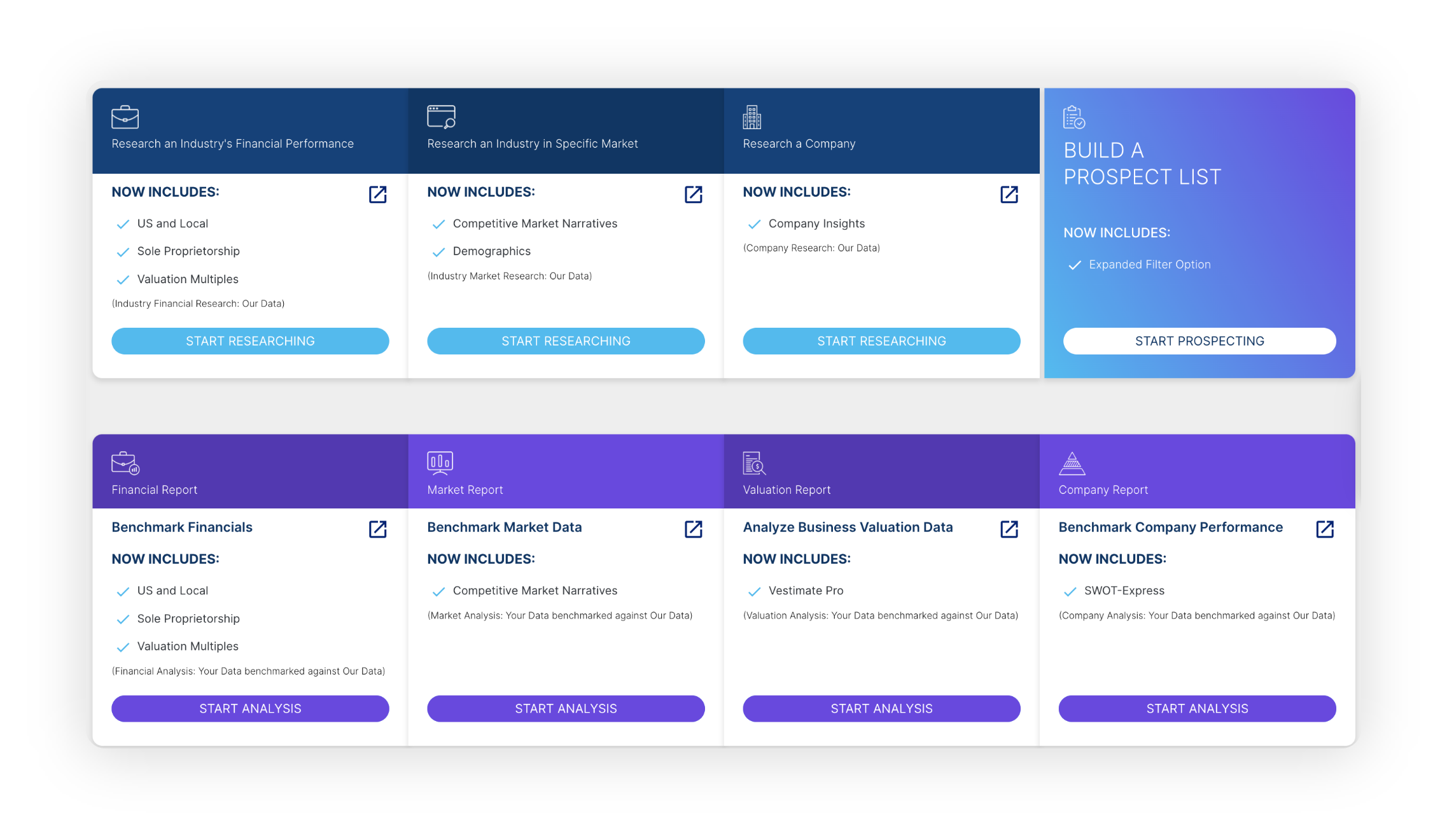

We ensure accuracy with our data by leveraging trusted sources, gathering billions of data points from the web, public, and private databases, and maintaining a robust quality control system that includes test projections. Due to the reliability of the sources and the volume of data available we use to create profiles and reports, we can provide more reliable insights than any other provider. Bizminer is widely accepted for industry analytical work, benchmarking, valuations, forensics, taxes, and litigation.

Our Taxonomy

Bizminer reports apply a system that we have developed to classify and report on industry segments. In addition to the standard North American Industrial Classification System (NAICS), we get even more granular by representing specialty industry segments under NAICS-6 industries, incorporating a decimal point and up to eight digits after the decimal in results.

The Most Up-to-Date

Our data is the most up-to-date of all providers. Data is updated dynamically as soon as it’s available from our public and private sources, ensuring you have the latest insights. When you pull a profile or report, your query will initiate a new search to pull in the most recent information available.

See how Bizminer's superior data sources, methodology, and taxonomy help you make better business decisions.